Burlington residents can afford properties in these cities

Published August 15, 2024 at 9:29 am

It’s tough to save for a new home while you’re stuck with paying the rent, but an online real estate company has an idea for Burlington residents.

The term ‘rentvesting’ is gaining popularity in real estate circles.

According to Zoocasa, rentvesting is an equity-building strategy where you purchase a property in a more affordable city and rent it out to earn investment income, while simultaneously renting a home in a typically more expensive city where you prefer to live.

After a few years of earning monthly income from your tenants and building equity in your investment property, you can sell it and use the gains for a down payment on a home in your desired city.

When looking at opportunities, Zoocasa calculated the maximum mortgage amount the average income in Burlington could afford. They then analyzed average condo apartment prices across Canada, comparing the average rent and the average monthly mortgage payment in each location to determine where Burlingtonians could afford to buy and where investments would potentially be profitable.

With an average annual income of $66,100, a homebuyer from Burlington can comfortably afford a mortgage amount of up to $293,378.

With a total average mortgage amount of $292,720, investment buyers from Burlington can afford to purchase a condo apartment in Moncton.

Moncton was ranked as the top city to buy real estate in 2024, due largely to the city’s consistent economic growth, with home values appreciating by 98 per cent over the past five years.

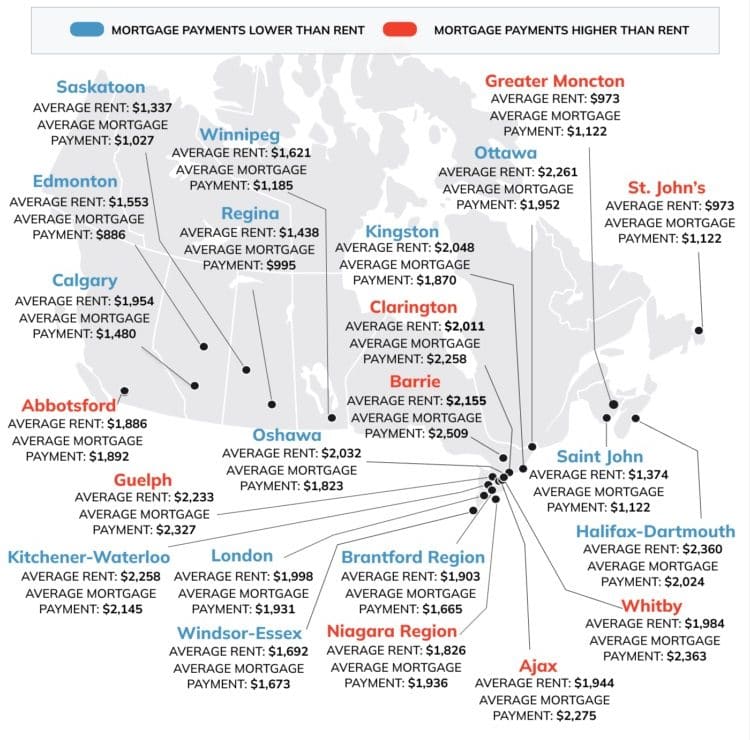

In 14 cities across Canada, a condo investment property has the potential to earn monthly gains thanks to the average rent being higher than the average monthly mortgage payment.

For buyers from the GTA, this means an opportunity to not only profit from their investment but also potentially cover their own monthly rental payments.

This additional income can help them save more effectively and ultimately afford their own home in the future.

Edmonton offers the highest profit potential, with average rents at $1,553 and average monthly mortgage payments at just $886, resulting in potential monthly gains of $667. Calgary is the next best option, with the average rent at $1,954 and the average monthly mortgage payment at $1,480, which is $474 below the average rent.

Other cities with potential monthly gains exceeding $300 include Regina, Saskatoon, Winnipeg, Ottawa, and Halifax-Dartmouth. While the total mortgage in some of these cities, such as Halifax-Dartmouth, might be higher than what the average income in Toronto can afford, the potential monthly gains can make the investment worthwhile.

Before you take the plunge, make sure you know the ins and outs of the process. Obtaining a mortgage for an investment property is slightly different than obtaining a mortgage for a residential one.

Compared to a traditional mortgage, a mortgage for an investment property requires a higher down payment and can have stricter credit score and debt-to-income ratio requirements.

It’s also important to note you cannot use funds from your First Home Savings Account to buy an investment property, as these are only allowed for the purchase of primary residences.

However, you may be able to qualify for special tax deductions, such as being able to deduct mortgage interest, property taxes, insurance, and maintenance costs from your rental income.